I never said "production". I said "supply". For a guy who is tossing around "Econ 101" quips, you would think you would know the difference.fixer said:aTmAg said:When the supply curve moves down the equilibrium point moves right in addition to down. A more right equilibrium, point means a larger quantity. So if they don't want to lose money, then they better increase their production. If they do not, then somebody else will. Even if they have to enter the market to do so.fixer said:aTmAg said:I never said supply would magically go up. I went out of my way to to say if we "double their production" to make it clear that I was talking philosophical. Of course, I do not think we can snap our fingers and double their production in an instant. Nor did I say that prices would go below equilibrium. The equilibrium price would become much lower.fixer said:

See my edit.

Supply just can't magically go up. The market forces seek to balance supply and demand. Prices reflect this.

Producers seek to maximize profit while consumers seek to reduce costs.

A producer is incentivized to make more by higher profits. One aspect is a higher selling cost. Another is lower cost input materials and resources.

Producers will make a certain amount of product for a certain price. Consumers buy a certain amount of a product at a certain price.

If supply goes above this equilibrium the prices tend to come down because it is an incentive for consumers.

The equilibrium aspect in supply and demand is missing in your assumption that a simple increase in supply ( apparently of all or most goods) will lower costs.

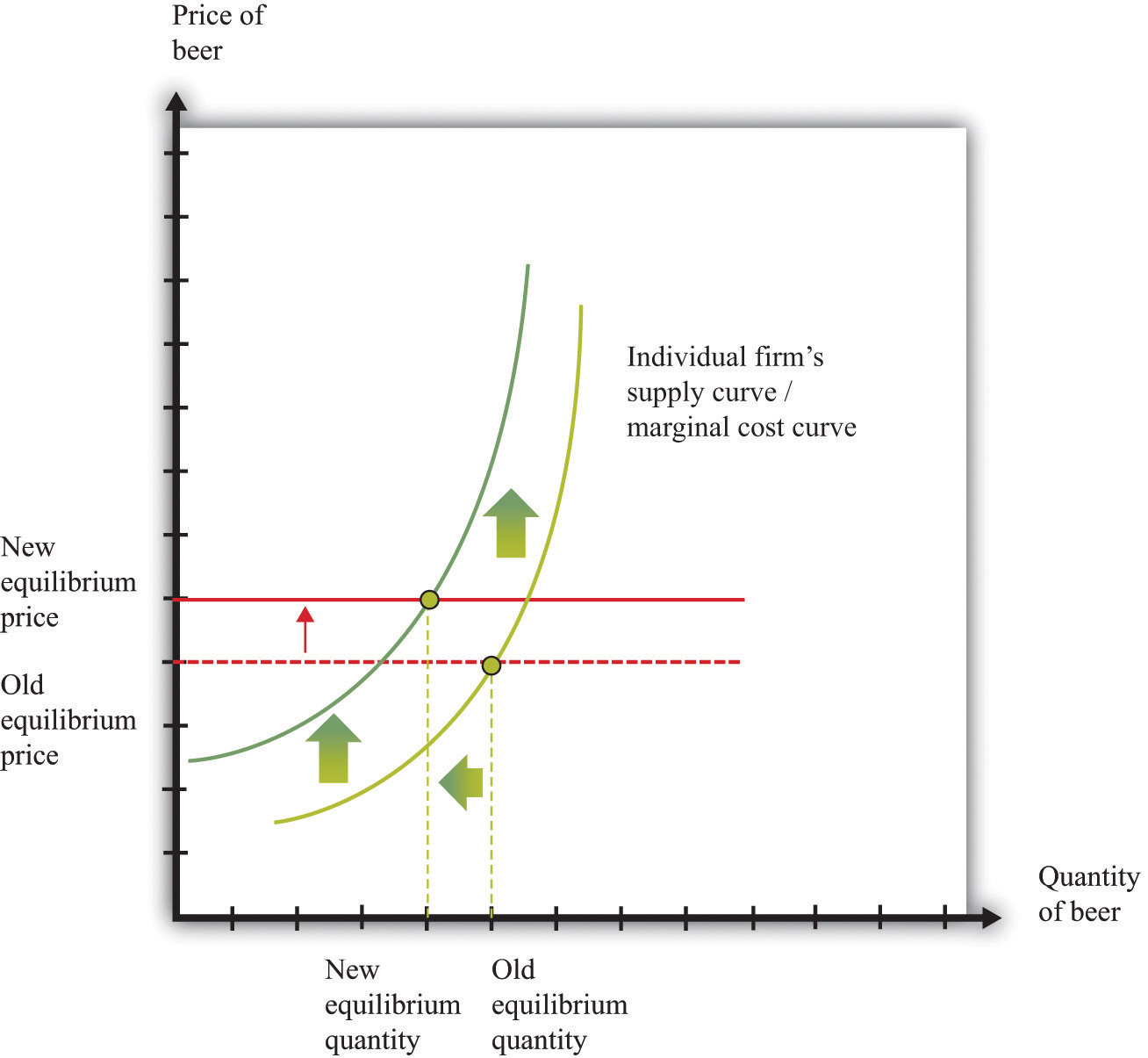

If government stopped welfare then that would greatly reduce salary requirements since people who now refrain from working for any offers lower than X will get off their asses and work for vastly lower salaries in order to not starve. Since salaries are the top expense in most businesses, suddenly entire industries that are unsustainable in America now would become viable again. That would move the supply curve right lowering prices. In addition, since everybody would be paying lower salaries, competition would also push the supply curve down and prices lower until it reaches equilibrium.

Ok so I was with you on lower input costs for labor.

But if a company lowered their input costs they aren't going to simply ramp up production. There has to be a signal for increased demand.

This is all true and is also not the same thing as " increasing production will lower prices".

To argue that a larger supply does not push down prices is like arguing that the world is flat.